Why Aggregators Fail

Amazon aggregator, Thrasio, preparing to file for bankruptcy

"Failure of business schools to study men like Singleton is a crime.” - Warren Buffet

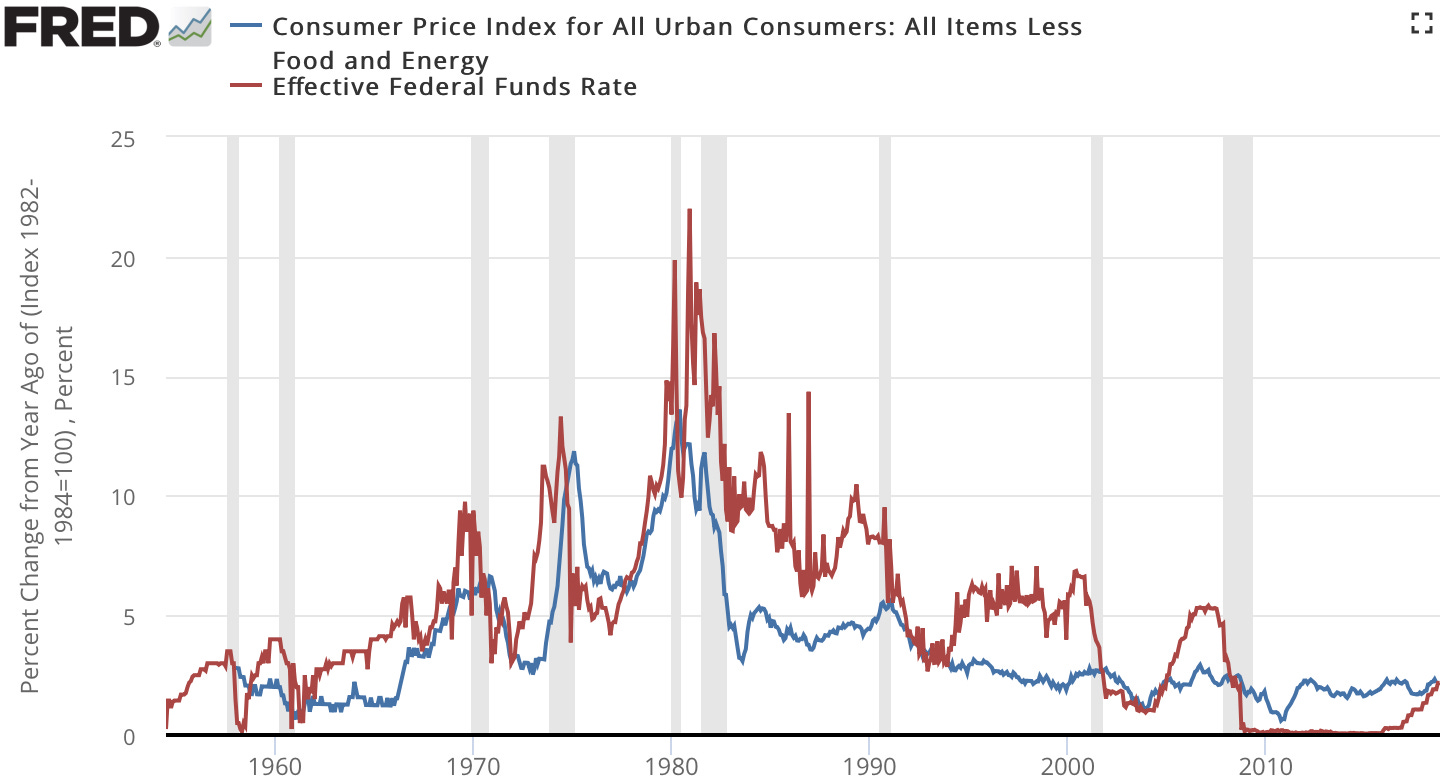

The first meaningful conglomerate boom occurred in 1960s. Low interest rates (highlighted below) made leveraged buyouts (LBO) easier; enabling managers of large companies to make a case for category-agnostic acquisitions to bolster their valuations.

A conglomerate is typically a large company comprised of many independent businesses in which the conglomerate owns a meaningful stake. The conglomerate thesis was built around decentralized organizations that can manage risk and diversify across different sectors.

Before Private Equity (PE) became ubiquitous, we had conglomerates doing LBOs. PE was started post-WWII as a way to diversify capital risk and drive alpha, but it didn’t gain full traction until the 1980s.

Let’s take a dive into Henry Singleton’s background and what made him a great capital allocator.

Henry Singleton and Teledyne

Warren Buffet describes Henry Singleton as having the best operating and capital deployment record in American business. But who is Henry Singleton?

Singleton was an engineer turned entrepreneur who built Teledyne, one of the most successful conglomerates of all time. He co-founded the business and remained CEO from 1960 to 1986. In the first 9 years of his tenure, he acquired 130 companies ranging from insurance and aviation to electronics and specialty metals. He took full advantage of the financial arbitrage capital markets were providing and was rewarded handsomely.

He never acquired businesses that required turnarounds or restructuring. Always focused on buying profitable companies that were growing in niche markets. When rates were low, Singleton would buy-back Teledyne stock. He preferred to not pay dividends given the lack of tax efficiency (dividends get double taxed).

Starting in 1970s, conglomerates began to struggle as interest rates climbed up. Remember, these were decentralized organizations allowing businesses to operate independently with HQ-style oversight. When rates go up, risk appetite gets compressed. Synergies become difficult to foster and the financial arbitrage that once enabled conglomerates to thrive became a Frankenstein to manage.

I’m often reminded of a famous Buffet saying:

“Interest rates are to asset prices as gravity is to matter.”

Why Do Aggregators Fail?

When rates are low, we see late cycle and speculative behavior by capital allocators.

")

Thrasio is the largest Amazon aggregator. They acquire Amazon FBA businesses and roll them up. Thrasio was started in 2018 and raised $3B+. It’s now planning for bankruptcy end of 2023.

There’s no shortage of Amazon aggregators. Here’s a great source from Hahnbeck:

Remember, the job of an aggregator is to acquire and integrate independent businesses into their platform. It turns out, most aren’t acquiring at all at the moment.

In 2021 from Thrasio’s CEO: "After 100 integrations, we're battle-tested," says co-founder and co-CEO Josh Silberstein. "We are closing more than a deal a week, and with each brand we onboard, we learn something new. At this point, our flywheel is not just proven - it is accelerating." Source PR newswire.

There’s no way anyone can acquire businesses that quickly and integrate them properly. The physics of these businesses doesn’t allow for it.

With significant capital raise comes high expectations. When you’re leading M&A at scale, you need to do the following to ensure vitality.

Integration strategy: The best Formula 1 drivers push their cars to the limit at 200 mph while steering and breaking tightly around corners. Similarly, the best managers don’t just brute force their way to growth. They take a long-term view across business cycles. A lot of horsepower without having the ability to steer will drive you into the wall. Capital is the horsepower, managing it is the steering ability.

Minimize complexity with bolt-on: You need synergy to make 1+1 = 3. Cross-sell and up-sell opportunities, back-office overlap, cost controls, and prioritizing free cash flow vs EBITDA, etc. You need many variables to align for bolt-on acquisitions to work. Minimize complexity by not acquiring in disparate categories.

Managing debt: When leveraged properly, debt is the greatest tool in business. On the contrary, it’s your worst enemy when growth slows.

Honest accounting: creative accounting tactics will lead to disaster. You have to be dialed in at the unit economics level. Most SMBs selling on Amazon won’t have the cleanest books. You have to run a quality of earnings to ensure proper reporting. And it’s tough to run a full M&A process when you’re acquiring a brand a week.

If you’re a founder thinking about selling to an aggregator or a strategic buyer, make sure you do your due diligence on them. Large acquirers will typically use their size and muscle to allure you into a transaction. Don’t fall for it. Be thoughtful. Recognize the hard work you’ve put into building your business. No one, and I mean, no one cares about your business as much as you do.

It feels like the late 60’s and early 70’s. Just like the conglomerates of that time struggled to make it through, aggregators are feeling a similar pinch.

History may not repeat, but it does rhyme.

This won’t be the last time we see an emergence of aggregators. During the next rate cut cycle, you’ll have a new set of aggregators emerge - signaling yet another late-cycle behavior seeking financial arbitrage.

Your style is brisk and your content is educative.