Letter # 1

Letter # 1

Fuel check, investing in equities, Amazon's impact on eComm and more

Happy Friday and welcome to letter # 1.

This has been a trying week for our country and our communities. It was tough to write and launch this letter at a time like this.

I did a fuel check on myself before kicking off writing this week and realized that I get joy and utility from creating / building / learning things. I wrote a short essay on doing a fuel check early this week.

Your inbox is precious, so here’s what you can expect in my letters:

Thoughts / reflections on topics ranging from startups, investing, commerce, tech, marketing and more

Lessons learned from interesting conversations

Personal development (we’re both going to be on a journey to build a version of ourselves)

Books, essays and links I’m reading, writing and discovering

Thoughts and reflections on investing (public markets)

Over the last 3 months, I’ve spoken to over two dozen people about their investing strategies; particularly in public markets. These are folks managing their own personal account (no wealth advisory firm involved). The biggest observation has been people’s desire to seek quick wins in a speculative market, navigate losses, and decisions were often influenced or made by reading headlines, fear of missing out so buying when prices are high and group thinking (i.e. following others).

I’m not a professional public markets investor, but there are few principles I’ve started to implement after studying Bill Ackman and Warren Buffet’s framework. So, as a result, here’s what I think about when investing in equities:

Invest in businesses that I easily understand

Invest at a reasonable price

Invest in a company that could theoretically last forever

Invest in a business I would actually want to own and be proud of

In reality, when you’re buying stock, you’re buying part of a company; you’re an owner in that business. You just have other people operating it. I think everyone reading this understands that, but when making speculative buys, we forget it.

More specifically, when I look at the “value sector” in my portfolio, I study the balance sheet before making the investment.

To go deeper in the thought process, let’s explore an example. I recently bought some Southwest Airlines (LUV). The decision to buy came down to:

Financials

Company’s cash on hand

Operating income change QoQ and YoY

Net revenue change QoQ and YoY

Comps

Observe financials for AA, Delta, JetBlue, etc and see how LUV is doing relative to others

Macro environment and consumption behavior

LUV is a domestic airline; International travels will impact top line revenue for many airlines

Has an incredible brand that people love

Well-managed and has a people-first culture

It’s not for corporate travelers

Bags fly free… they don’t nickel and dime their customers

Great rewards program to activate customer acquisition

… And finally, people will fly frequently again

I bought the stock at $28.09 per share. Looking at the last 5 years, stock has been relatively steady (minus short term COVID impact) and above the amount I paid for it, so it feels like a reasonable price to pay. I should’ve bought more, so that’s likely my only regret.

Again, I’m not a professional investor and have made many mistakes. I would encourage anyone reading this to do their own diligence before making any investment decisions. I hope the framework shared above can be helpful as you evaluate opportunities.

Thoughts on state of eCommerce and Amazon

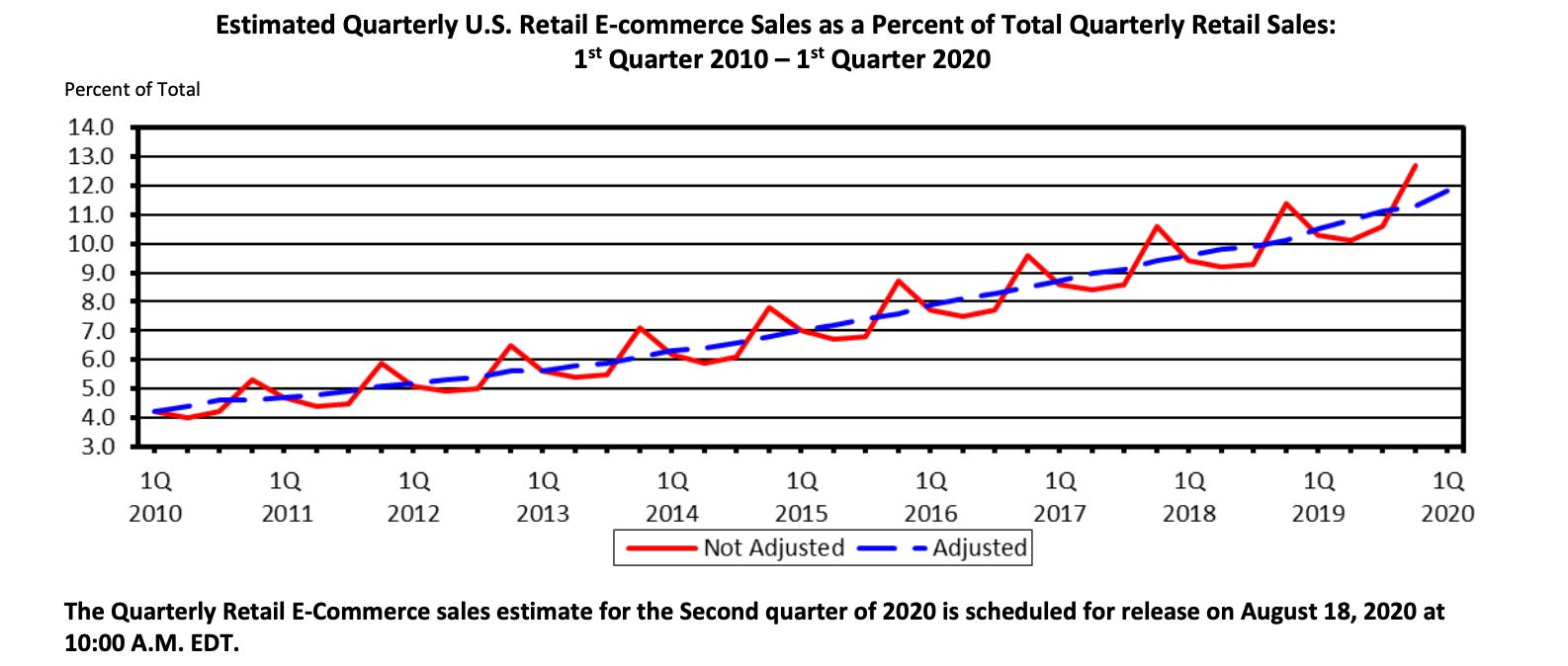

Q1 2020 paved the way for eComm. The latest U.S. Census report shows Q1 eComm was only 11.8% of all retail sales ($160.3B eComm of total $1.36T of all retail sales).

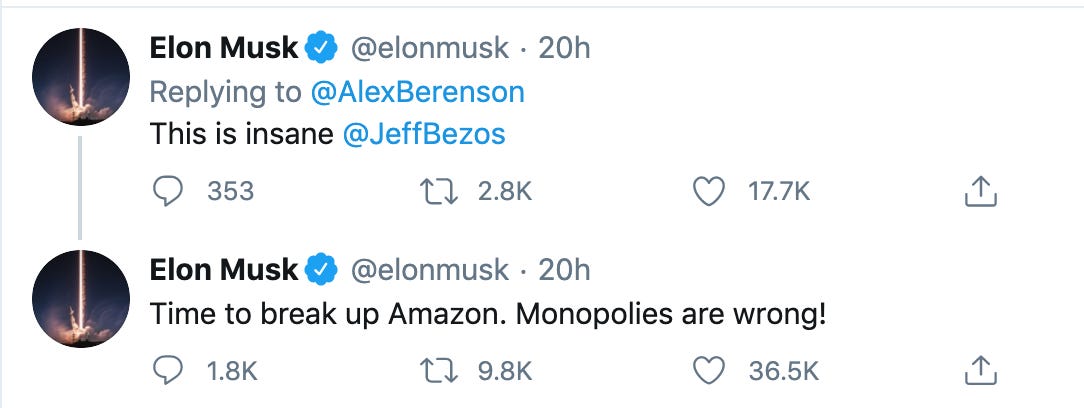

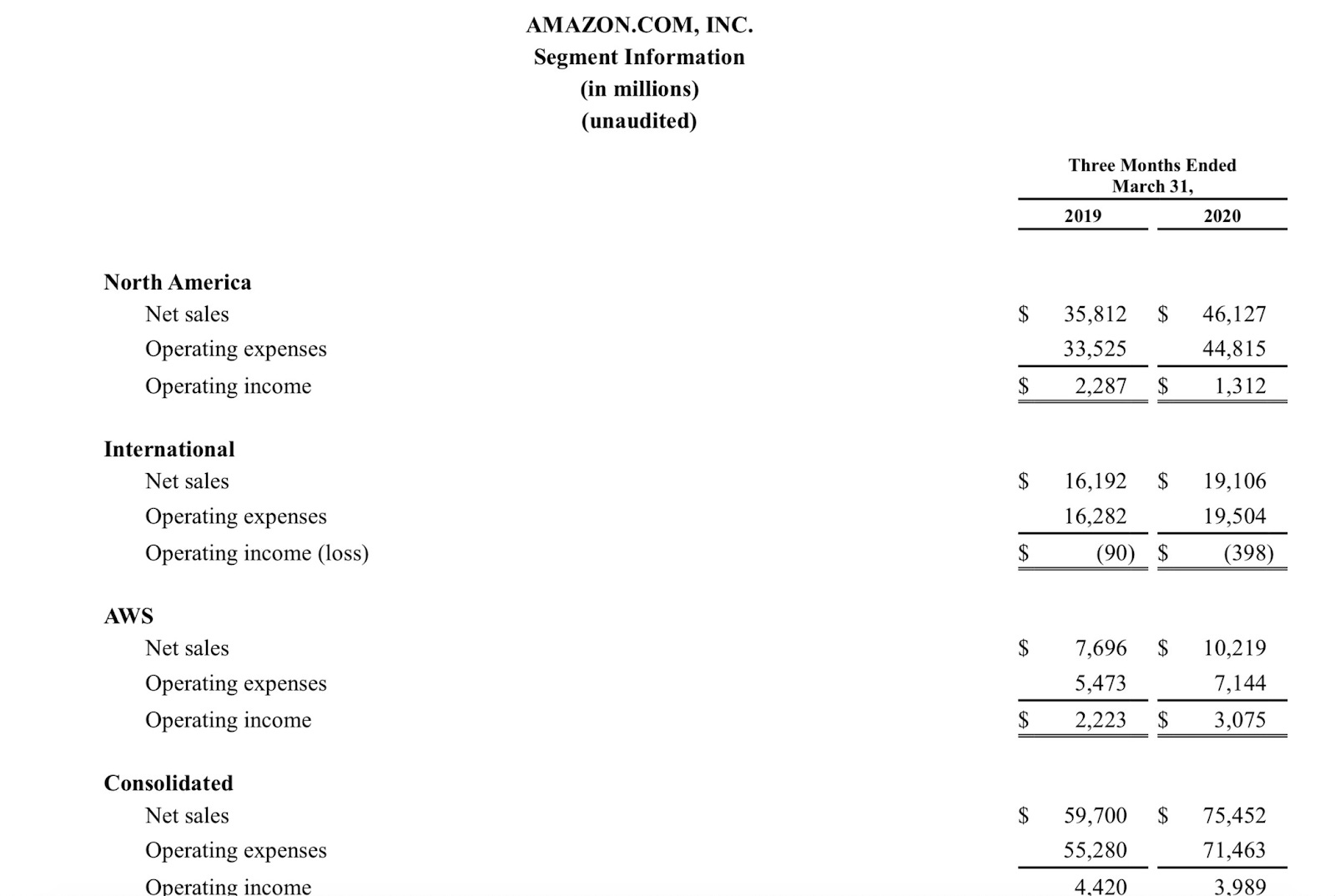

Amazon net sales in North America (excluding AWS business) was ~$46B. Amazon earned ~$21.3M per hour in North America. Amazon is ubiquitous and these numbers are incredible… Perhaps Elon is reading Amazon’s financials in detail and tweeting about it.

… not really. Elon is just upset about Amazon fact checking his upcoming book on COVID-19 and not meeting their guidelines.

Back to eComm. Data suggests that Amazon is 25-30% of all US eComm. This is a strong signal that the long tail effect of independent consumer brands is real.

There are some data sets that don’t exclude AWS and international sales when looking at Amazon’s impact on US retail. Functionally, it’s only 2-3% of all US retail, and it’s clear that Amazon’s business is collectively much bigger than just its eComm arm.

Now, let’s explore the future of eComm. It’s on track to have a record year. COVID-19 isn’t just a change agent; it’s an accelerant for the vertical. Things we were suppose to observe in the next 5 years, we will observe in the next 10 months. It’s paved the way for up starts and incumbents that invested in digital. 11.8% impact noted above is for Q1. COVID became a real thing when countrywide quarantine went into effect in mid-March. We’re more than 70% of the way through Q2 and the world looks and feels much different now than it did in Q1.

I’m expecting Q2 eComm sales to be ~23% of all US retail sales. Some early signals and research is suggesting that it’ll be close to 27-30%. US states opening earlier than expected can influence eComm penetration in the short term.

Let’s zoom in for a moment. I’ve personally observed incredible growth in direct to consumer (DTC) brands over the last 8 weeks. I’m talking 500%+ type growth in top line revenue while maintaining healthy operating margins. The smartest decisions these brands made were tackling inventory constraints earlier in the year and doubling down on marketing.

This spark, however, is not steady-end state. June will be a trying month for many companies and independent brands. It will not look similar to the success seen in April and May. Reasons range from retail opening up, broader employment uncertainty, social unrest… all those things impact consumer behavior.

Amazon’s current guidance suggests that it’ll do $75-81B in Q2 in total sales. All else equals, they’ll likely do $45-51B in net sales in North America (excluding AWS). Which means independent eComm brands will own a much larger share of eComm pie in Q2. Combined impact could be Q4 2019 + Q1 2020 combined.

Dynamic nature of COVID-19 makes forecasting challenging. As we get into earnings season in a few weeks, we will observe many traditional retailers explicitly reporting on their eComm revenue as a % of total sales. This will be an attempt to signal innovation and resiliency. But it should be taken with a grain of salt. E-commerce cannot replace offline revenue for traditional retailers.

Parting thoughts

I intend to write letters weekly but it may vary… schedule can be fairly compressed depending on the week. My focus will be on quality and to respect your inbox.

If you enjoyed this letter, please share it with colleagues and friends. Link to subsribe.

Thank you.