How to Think About Debt

ABL, LOC, term loan, venture debt and more

This essay is for founders navigating the operational complexity that comes with scale.

You’ve built a high-growth business. You’re working to create meaningful infrastructure: dialing in inventory cycles, creating operating leverage by running lean, managing freight volatility, and have de-risked some of the operational friction that comes with scale. You’ve likely implemented a rolling forecast, actively stabilizing your contribution margins, and negotiated vendor terms to extend payables. But if you haven’t proactively designed your capital structure to absorb timing risk and cash conversion mismatches, you’re carrying a hidden liability on your balance sheet. One that won’t show up in the P&L until it’s too late.

Because while growth hides problems, debt reveals them.

My firm has the privilege of looking at many companies each year. We get exposed to over $1.5B+ in GMV annually. As a result, I see many ways in which companies manage their working capital cycles. I’ve seen brands using term loans to patch inventory gaps, revolving credit to fund opex, or revenue-based financing to plug structural burn. On paper, it works. In practice, it compounds fragility. Poorly structured debt doesn’t just increase the cost of capital; it erodes cash runway, restricts flexibility, and can force suboptimal decisions when the plan misses.

I spend a lot of time speaking with founders across different sectors about optimizing the capital stack. I’m compiling my notes in this one essay to make it easier for others to reference. It’s designed to be a strategic guide for operators in the messy middle and capital-intensive businesses.

I’ll aim to unpack how to think about (and use) different types of debt products for your company.

But First, The Real Cost.

Let’s start with an example.

You just shipped a $2 million wholesale order. You paid the factory 30 days ago. The retailer pays in 75. Meanwhile, your DTC funnel is humming, but ad spend is front-loaded, and LTV payback is 60 days out. Your top line is growing, but your cash balance isn’t.

That gap between GAAP profitability and actual liquidity? That’s where debt lives.

Remember, debt is a tool in the toolbox. Done well, debt smooths the timing. Done poorly, it suffocates growth.

Besides contribution margin problems, the biggest mistake my team sees is brands using the wrong type of debt for the wrong job. Example of suboptimal usage:

Using term debt for working capital gaps

Using revenue-based financing (RBF) to plug in structural burn

Using line of credit (LOCs) to fund long-term initiatives

Each of these errors creates silent fragility. They don’t always blow up in Year 1. But they quietly compress flexibility until the next macro shock (or the next bad quarter) forces your hand.

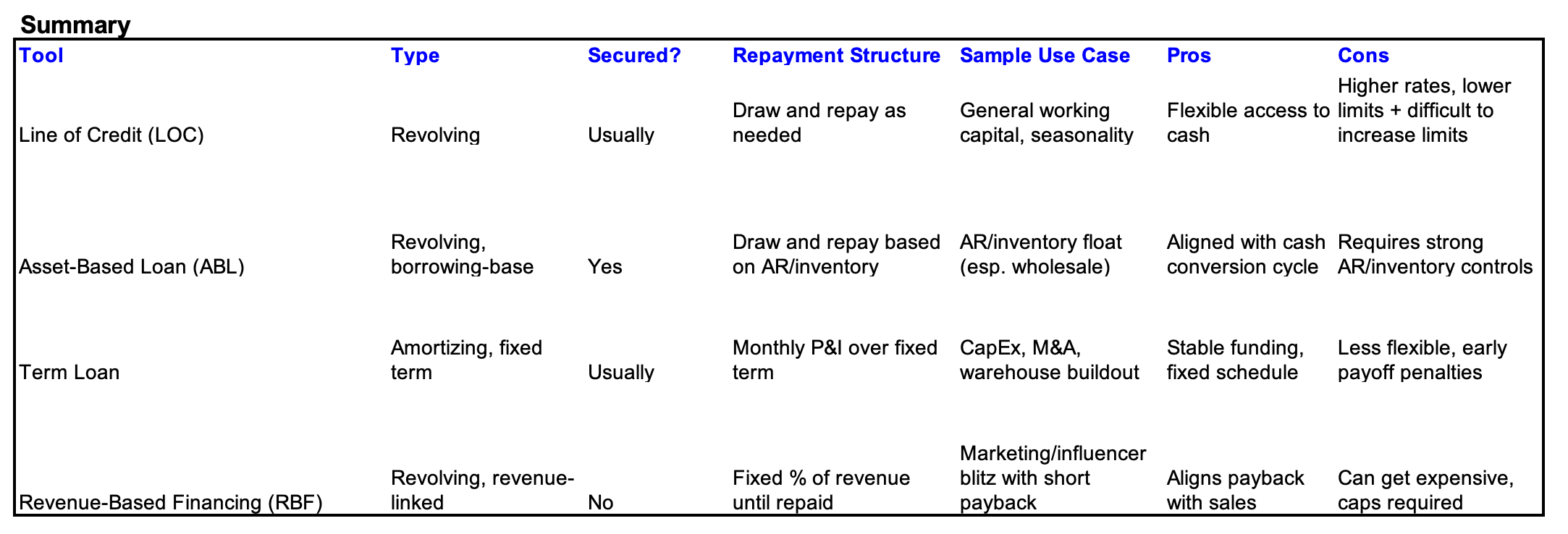

ABL and LOC: Working Capital Gap Buffer

Let’s explore further.

LOC is a revolving facility secured by your short-term assets, typically AR and inventory. It’s designed to bridge the timing mismatch between cash out (to suppliers) and cash in (from customers). Draw, repay, redraw.

An asset-based loan (ABL) is a secured LOC collateralized by assets and is calculated on a borrowing base (e.g. 85% of AR and 50% of inventory).

LOC is a broad credit product. An ABL is a specific type of LOC. In other words, all ABLs are like LOCs, but not all LOCs are ABLs. ABLs are more structured and monitored, with borrowing base certificates, field exams, and tighter controls.

I generally lean into ABLs for companies that have the borrowing base. It scales nicely as the balance sheet expands.

When it works well:

You ship wholesale POs with 30–90 day terms

You buy inventory ahead of seasonal demand

Your business has a recurring, but lumpy cash flow pattern

This is not growth capital. It’s working capital.

Here are the mechanics:

Borrowing Base: Usually 85% of eligible AR, usually 50% of eligible inventory

Interest: Floating rate (SOFR + spread). Typical range today: 9–12%. Varies greatly depending on lender (nonbank credit can be more expensive but has more flexibility)

Lender: Banks if you’re larger and profitable (more conservative). Non banking ABLs (more flexible and creative in deal structures)

Covenants: Leverage ratios, fixed charge coverage, sometimes springing PGs

Reporting: Monthly borrowing base certificates, regular audits, close attention to AR aging. You need to ship the credit pack monthly.

Smart Use Case

You ship a $5M Target order with 60-day terms. You need to pay your supplier now. An LOC lets you borrow $4M (80% advance rate), pay the factory, and repay when Target pays you.

Where It Breaks

You start using it to fund marketing or fixed costs, or OPEX in general.

Lenders typically have covenant requirements for use of proceeds. You can only use it to finance working capital gaps, not opex or capex.

You’re always maxed out and repaying just enough to redraw

Inventory ages out, reducing availability unexpectedly

One big AR gets delayed and your borrowing base collapses

If your LOC balance isn’t moving and only increasing, you’ve stopped floating.

Most ABLs will have terms in their loan service agreements (LSA) on use of proceeds.

Term Loan: Long Term Capital for Long Term Use

Term loan a lump sum of capital repaid over a fixed period, typically 24-36 months. It comes with a set amortization schedule and often requires hard or soft collateral. You use it to build something that will pay off over time, not to fix short-term imbalances. Here’s when it works well:

Capex: new warehouse, machinery, ERP build

Acquisitions: buying a smaller brand, consolidating a supplier, verticalizing the business

Debt Refinancing: replacing expensive or misfit debt with cheaper, longer-term capital

Here are the mechanics:

Amortization: Fully amortizing, or interest-only with a balloon

Rates: Typically 9–15% for private credit; lower for asset-backed bank term loans

Collateral: Equipment, property, or general business assets

Covenants: DSCR, EBITDA minimums, leverage ceilings, and more

Structure: Can blend with equity for larger strategic moves (e.g., 70% debt, 30% equity for an acquisition)

Important to note: for companies that already have a senior credit and subordinate, private credit is typically available to you on MOIC (multiple of invested capital), which is a fee that’s associated with the credit product (this is different than standard APR calculation), and fees are normally priced into the product. The hurdle rate for MOIC is decided by the creditor and it can vary. It’s not cheap, but does have flexibility built into it. This trade off requires proper mapping of cash flow forecasting.

Smart Use Case

You’re building a $4M warehouse to consolidate 3PL spend and improve shipping speeds. It will pay back in 2 years via margin lift and customer satisfaction. A 3-year term loan lets you match asset life to liability duration.

Where It Breaks

You use it to cover losses, hoping growth solves the problem

Revenue is seasonal, but payments aren’t

ROI from the investment lags, and you’re stuck making payments without the payoff

You’re 20 months into the loan and the asset hasn’t delivered cash flow. Now you’re servicing debt off your base business, not from the intended ROI.

Revenue-Based Financing (RBF): Fast, Flexible, Expensive

RBF gives you upfront cash in exchange for a share of your future revenue until a fixed cap is hit (usually 1.0x to 1.6x the amount borrowed). Payments flex with sales, so you pay more in strong months and less in slow ones.

It’s technically not a loan; it’s a purchase of receivables. But it behaves like variable-cost debt.

Here’s when it works well:

You’re running a high-ROAS campaign with proven LTV/CAC models

You need a short-term boost for inventory restock with rapid sell-through

You can repay in 3–6 months and understand the true cost

Here are the mechanics:

Payment: 5–10% of gross revenue until cap is hit

Cost: Effective APR varies wildly—can be 20–50%+

Speed: Often funds in 7–14 days (fast)

Lenders: Non dilutive merchant cash advance players (MCAs)

Risks: No covenants, but might come with PGs or restrictive side letters. They may also come with inter-funding agreements with senior creditors or springing UCCs.

Float: Daily/weekly cash sweeps. This requires thoughtful liquidity planning.

Smart Use Case

You’re launching a product drop with pre-orders or strong historical velocity. You take $500K in RBF, deploy it to paid media, and recoup in 90 days at a 1.25x repayment cap. High cost, but fast ROI.

Where It Breaks:

You use it to plug holes in structural burn

You take multiple tranches and layer repayment obligations

You forget it’s eating into gross margin like a phantom COGS

You’re paying 10–15% of revenue across 3–4 RBF providers. Gross margin looks fine on paper, but operating cash flow is collapsing.

Experience share: This can become an energy vampire. When brands have bolted on multiple RBF products and then have to help clean up the balance sheet over a short period of time. It’s like doing a spine surgery on a patient who also has stage 2 cancer. It’s tough.

Keep it simple. If you’re qualified for bank debt or standard ABL products, bring them on the capital stack, subordinate with other high quality credit accordingly. Ensure your balance sheet ratios are rock solid. And if you need additional RBF support, consult your CFO (make sure they’ve mapped out a strong liquidity plan and forecast), and then explore next steps.

A great capital structure isn’t just about cost of capital. It’s the one that doesn’t snap when reality deviates from plan.

How I’ve Seen Companies Get This Wrong:

Using Debt to Fund Burn: If your GM% doesn’t cover SG&A, no debt instrument can save you. Debt doesn’t fix broken unit economics, it just delays the reckoning.

Overloading RBF: two rounds is fine. Five is a slow bleed. As you layer tranches, you layer repayment drag. Suddenly, you’re working for the lender, not your equity.

Ignoring Cash Flow Modeling: You need a surgical 13-week cash forecast. Every debt obligation should be stress-tested. What happens at 80% of forecast? 60%?

Misaligned Debt Duration: Using short-term debt to fund a 3-year initiative is the fastest way to a refinance crisis.

Debt Is a Strategic Tool (If You Know How to Use It)

Debt isn’t good or bad. It’s just a tool in your toolbox. It can be powerful. But power without fluency is a liability.

The best capital allocators I know don’t just raise money; they engineer capital stacks that absorb shocks, amplify upside, and preserve optionality. They know that matching repayment mechanics to cash generation is the difference between financial flexibility and fragility.

Mastering debt (and your capital stack) won’t get you applause. But it’ll keep you in the game when your competitors are forced to fold.

P.S. What Else is Out There?

Beyond the big 4 above, here are a few other debt instruments all founders should be familiar with:

Venture Debt: These are structured term loans offered alongside or shortly after equity rounds, typically by specialized lenders (e.g. SVB). It’s underwritten based on your VC’s backing and your last round valuation, not your cash flow. It’s useful for extending runway, but often includes warrants and tight repayment timelines.

We run into venture debt options frequently post capital raise. Here’s a simple cheat sheet:

Mezzanine Debt: This is hybrid capital that sits between senior debt and equity. Typically unsecured, with higher interest rates (12–20%) and sometimes equity kickers or warrants. Best used for acquisitions or growth-stage capital when you want to preserve equity but can’t secure more senior debt. High-risk, high-reward, and usually reserved for companies with stable EBITDA and a clear exit path.

Convertible Notes & SAFEs: This is more common in early-stage or venture-backed companies, these are technically equity instruments that behave like short-term debt. They defer valuation negotiations and convert into equity at the next priced round. Founders should use them carefully; esp when bridging into uncertain capital markets environment.

These instruments have their place, but they require sophistication, financial fluency, and a clear view on exit or next funding milestone. When in doubt, build the foundation with core credit products first, and treat these as optional layers, not default tools.