History of Interest Rates

Debt is a tool that, when leveraged properly, can be powerful. Interest rates are established by central banks; in the United States, The Federal Reserve Bank controls monetary policy and influences fed funds rates - the rate that banks can charge borrowers.

Interest rate swings influence many things. Common use case for leverage includes everything from real estate to building bridges and factories to buying stocks and acquiring companies.

Here’s a fascinating chart capturing the history of interest rates last 700 years.

We’ve been living in a declining interest rate environment for 40+ years, with lowest points reached in 2020 due to COVID. In fact, we’re at lowest rates in last 700 years. It’s never been cheaper to borrow money.

If we zoom in a bit, we notice an interesting trend: interest rates tend to go through cycles, just like everything else. The cycle is normally 50-60 years of rise and fall.

During WWII, we saw rates falling to ~2%. Government spending was up meaningfully. If you look ahead to late ‘70s and early ‘80s, you see rates hitting all time high. Mortgages were at 14%! Hard to fathom that today. That was also a time of high inflationary pressures.

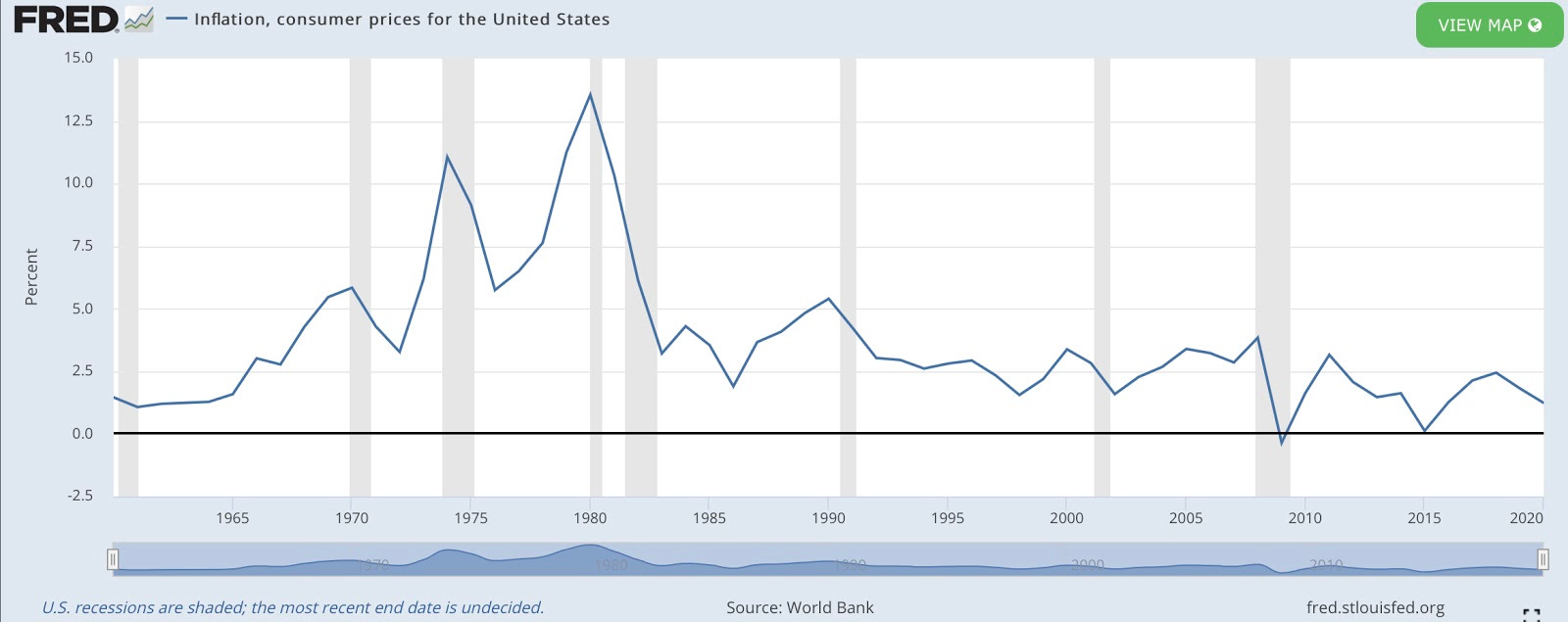

It’s important to understand the inverse relationship between interest rates and inflation. When inflation rises, interest rates normally fall. And vice versa.

Inflation is on the horizon. All signs are pointing to this. We’re seeing it in home prices, used car market, commodities, natural resources and pretty much everything else.

Inflation hurts purchasing power. It evaporates savings and devalues cash. A steady 2% annual inflation can be healthy for the economy, but the Fed has to strike a healthy balance… current monetary policy efforts of printing too much money can have substantial consequences.

Interest rates are a tool that The Fed has to control inflation. Influencing Fed Funds Rate is a way to reduce borrowing power and over time controlling prices; albeit the current Fed has little desire to increase rates. They’re laser focused on quantitative easing (QE) and getting the economy back on track.

As we look into the next 10-12 years, we can expect the opposite of what we experienced the last 40 years: interest rates going back up. It feels like “this time is different,” but it isn’t. We’ve seen these swings for the last 700 years. And certainly since the Fed became an entity in 1913.

History tells us that rates ebb and flow first few years of a rise and then experience a sharp spike in a short time window.

So, what does this mean for retail investors? Well, for one, home prices increasing are directly correlated with interest rates being low combined with a surge in demand. When interest rates go up, demand will come down. Home prices will come back to equilibrium. Low rates are a good time to refinance your home since you’re locking in a fixed rate for the next 30 years.

Higher interest rates can also reduce market speculation by institutional investors. Hedge funds can’t afford to be over-levered. Since the cost of debt is high, risk management becomes paramount.

Precious metals like gold and silver perform okay when inflation is high; opposite is true when it isn’t. Precious metals are normally a hedge against inflation. Commodities, natural resources, amongst other things tend to perform poorly when rates are high.

When rates are rising, banks and financial institutions perform better. It allows them to make more margin on loans and other transactions.

Value stocks become more desirable than growth stocks. Bonds do not perform as well when rates rise. Bond prices normally drop when rates go up.

The list goes on.

Jerome Powell is committed to QE efforts and keeping interest rates low for now. But this can change and likely will if we study history of interest rates. It’s always good to understand macroeconomic policies and how it can impact your portfolio.

References:

Visual Capitalist published by Nicholas LePan

Royals Investment Advisor LLC.

St. Louis Fed, Inflation and consumer prices

Anything covered in this essay is reference material only and not financial advice. Please consult a financial advisor before making investment decisions.